Bitcoin

/

Bitcoin (BTC), the cryptocurrency, is supported by a network of independent miners and is always mining blocks. Each block is a challenging computational problem, and the difficulty is adjusted based on the computational power of the entire network so that one block is mined every 10 minutes. The computer that mines the block (solves the problem) collects the transaction fees associated from any transactions processed in that block and, currently, 25 new BTC. So, given we can estimate the reward for mining a block (in BTC) and the amount of electricity the network spend mining the block, can we quantify the value of BTC in dollars (USD)?

Fundamentally, the value of BTC should be greater than or equal to the energy cost needed to keep the network running. If miners receive less value from the BTC they earn than from the electricity they put into mining they will leave the network, and the average amount of BTC each remaining miner receives will increase. If the value of BTC is excessively high compared to the electricity input miners will enter the network and the average amount of BTC each miner receives will decrease. The decision to enter or leave the market is unique for each miner, but we assume the long run average value of BTC in dollars is greater than or equal to the cost of mining. So mathematically,

(transaction fees + new BTC) = cost of electricity * energy input

The left hand side of the equation is the number of BTC per block. We have already covered new BTC. This amount of new BTC decreases by half every 4 years, and the last new BTC is expected to be awarded in 2140. So why mine blocks when no more coins are being awarded? When the block is mined, transactions are processed. These are other people, not necessarily the miner, exchanging BTC. If someone wants a transaction processed they attach a fee. These fees are awarded to computer that mines the block. In the long run individuals will only continue to mine if the reward, transaction fees, offsets the cost of mining, electricity costs. We will ignore capital and overhead costs (e.g. taxes, cost of buildings, miners, and labor) to simplify the analysis, but including these will increase the lower bound of dollars per BTC.

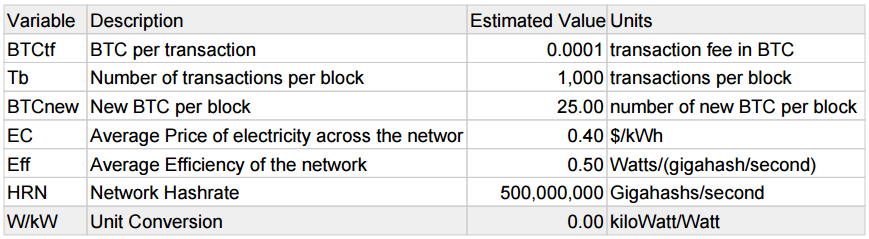

The right hand side of the equation is the dollars spent mining each block and relies on electricity being priced in traditional fiat currencies. A reasonable estimate for the average price of electricity across the network is $0.05/kWh. This is slightly less than the world average because large scale BTC mining is done in cooler climates to ease cooling costs or areas with cheap electricity. Energy input, like cost of electricity, is an average across the network. The energy consumption per Gigahash is continuing to improve, but current ASIC miners are estimated to consume 5 Watts/(Gigahash/second), also here. The size of the network, measured as hashrate, is readily available. Below are the variables used with estimated values:

We rearrange the first equation to get dollars per BTC. The 1/6 hour is assuming one block is mined every 10 minutes. This is not always the case.

$/BTC = (<EC> * <Eff> * HRN * kW/W * 1/6) / (BTCtc * <TB> + BTCnew)

With the assumptions above, the equation predicts $830 for 1 BTC. This is slightly above the current exchange rate of about $420. Indicating that BTC is currently undervalued relative to the resources used to make those BTC (the amount of electricity used to make BTC is greater than the worth of those BTC when converted into USD). The calculated exchange rate is quite sensitive to the average cost of electricity across the network and the average efficiency of the miners used. If the cost of electricity is instead $0.01/kWh the exchange rate drops to about 1BTC=$166. Similarly, if the miners are more efficient, say only 0.5 Watt/Gigahash, the exchange rate drops to only 1BTC=$83. Other explanations for people paying more in electricity than the value they get include people mining for fun, as insurance against holding centralized currencies, or expecting the value of BTC to increase dramatically. For example, after the next halving, expected in 2016, the reward of new BTC will drop to 12.5 per block, and the exchange rate predicted by the equation jumps to about $1,653. In the extreme case, when new BTC are no longer released and the only reward for mining is transaction fees, the exchange rate predicted is 1BTC=$208,000 (assuming the cost of electricity, mining efficiency, number of transactions per block, and transaction fees are the same in 2140 as they are today, lol). With the new BTC rewarded at zero, the hashrate of the network would have to drop to only about 500,000 Gh/s, from the current 500,000,000 Gh/s, for the exchange rate to be about today’s rate.

In the end, this was a fun exercise to put some numbers on the resources being put into BTC and compare those to the current value of BTC. This analysis suggested BTC is currently undervalued, but in reality, BTC's value derives from many different sources including an alternative to restrictive currencies, purchasing drugs, or protection against inflationary policy.